March 2, 2026

As we near the end of Q1, the mood across the credit union system feels noticeably different than it did a year ago. After several cycles of rate volatility, economic uncertainty and rapid digital change, recent surveys and industry polling suggest that both lenders and consumers are feeling cautiously optimistic.

Here’s what the survey results tell us – and where the opportunity lies.

Lending Leaders Like the Landscape

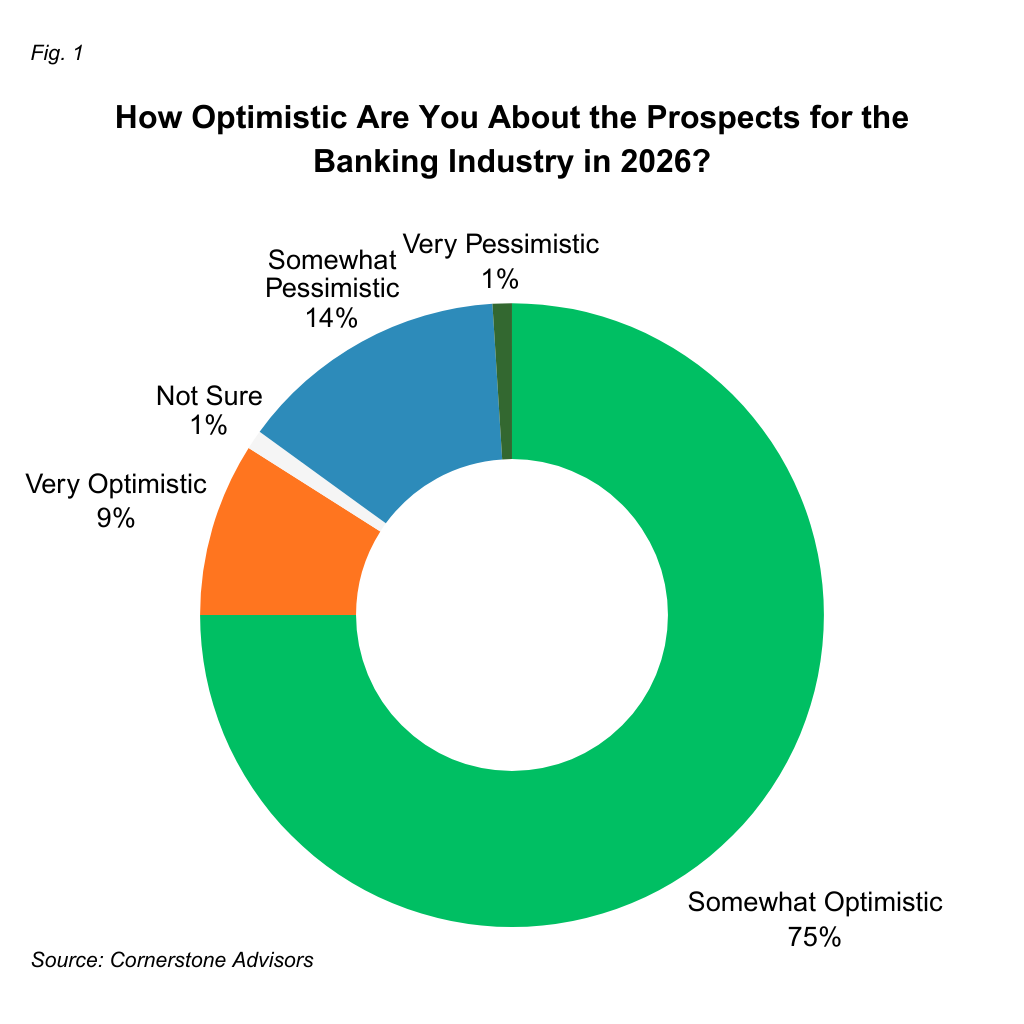

The new What’s Going On In Banking survey by Cornerstone Advisors found that more than 8 in 10 bank and credit union executives report feeling “very” or “somewhat” optimistic about 2026, and only 1% are “very” pessimistic.

This is a significant shift from the guarded outlook that dominated the conversation when LendKey spoke with the report’s author just last year. Why the change? Many respondents noted their optimism was due to interest rate trends, changing industry dynamics, new technology advancements and potential regulatory easing. Those who felt less positive noted uncertain economic conditions and the likelihood of increased charge-offs and delinquencies.

A similar tone appears in the Federal Reserve’s Senior Loan Officer Opinion Survey, where respondents said they broadly expect loan demand to increase across most categories this year. Lower interest rates, higher business investment and steady consumer spending are expected to support growth, even as institutions remain cautious around some types of consumer lending and credit quality.

A Vote of Confidence for Credit Unions

Encouragingly, confidence isn’t limited to the executive suite. A recent poll by America’s Credit Unions found that consumer sentiment remains strongly in favor of credit unions (73%), and 80% of those polled agree that Americans would be better off financially if more were to use credit unions rather than banks.

The reasons are consistent and telling: consumers value the not-for-profit, member-owned structure, competitive loan pricing, and visible community presence that credit unions provide. Transparency and fairness (qualities that can feel scarce in a digital-first financial world) continue to be key differentiators. Support for tax-exempt status is high (64%), and 94% back expansion into more communities and small businesses, reinforcing the idea that growth and trust are not mutually exclusive.

Balance Sheet Strategy = Competitive Edge

Where optimism can most rapidly turn into action, however, is through fintech partnerships.

With nearly two-thirds of credit unions already working with at least one fintech, these collaborations continue to expand; strengthening the system as they do by enabling credit unions to operate with increased speed and flexibility.

Of course, these partnerships typically require capital, too, so how credit unions manage their balance sheet is increasingly tied to their competitiveness. Put simply, when institutions want to lend more, launch new products, or invest in new partnerships, they need the capital flexibility to make those moves. This is where a partner like LendKey comes in.

Modern loan participation marketplaces can be a critical lever for a credit union looking to free-up or tie-up some assets. And despite the optimism, deposits are likely to remain flighty meaning margins remain sensitive. Having a flexible book can be the difference between merely staying afloat and strategically growing.

The Bottom Line

Despite economic uncertainties, both industry executives and consumers are signaling confidence. Credit unions enjoy strong public support, a growing suite of AI tools and fintech partnerships that expand capabilities. With the right strategies around technology, partnerships and product clarity, 2026 is shaping up to be a year of opportunity.

Talk to LendKey about how we can support your balance sheet management and seize the moment.